Personal vs Vehicle Breakdown Cover: Which One Gives You Better Value? Get Covered Online

A driver waits for help on a wet motorway hard shoulder, a common moment when breakdown cover suddenly matters, created with AI.

A driver waits for help on a wet motorway hard shoulder, a common moment when breakdown cover suddenly matters, created with AI.

It always happens at the worst time. The car won’t start on the drive when you’re late for work, or you’re stuck on the motorway with lorries thundering past. Sometimes it’s not even your car, it’s the one you borrowed, or you’re the passenger while someone else panics.

Find Breakdown Cover

That’s why breakdown cover is less about “nice to have” and more about avoiding stress and surprise bills. But there’s a common choice to make: personal breakdown cover (you’re covered in most vehicles you travel in) versus vehicle breakdown cover (that specific vehicle is covered).

This guide keeps it simple. You’ll learn which type is better value for your driving habits, your household set-up, and your budget (and why the cheapest option can still cost more in real life). Features and limits vary by provider, so the goal is to help you compare like-for-like.

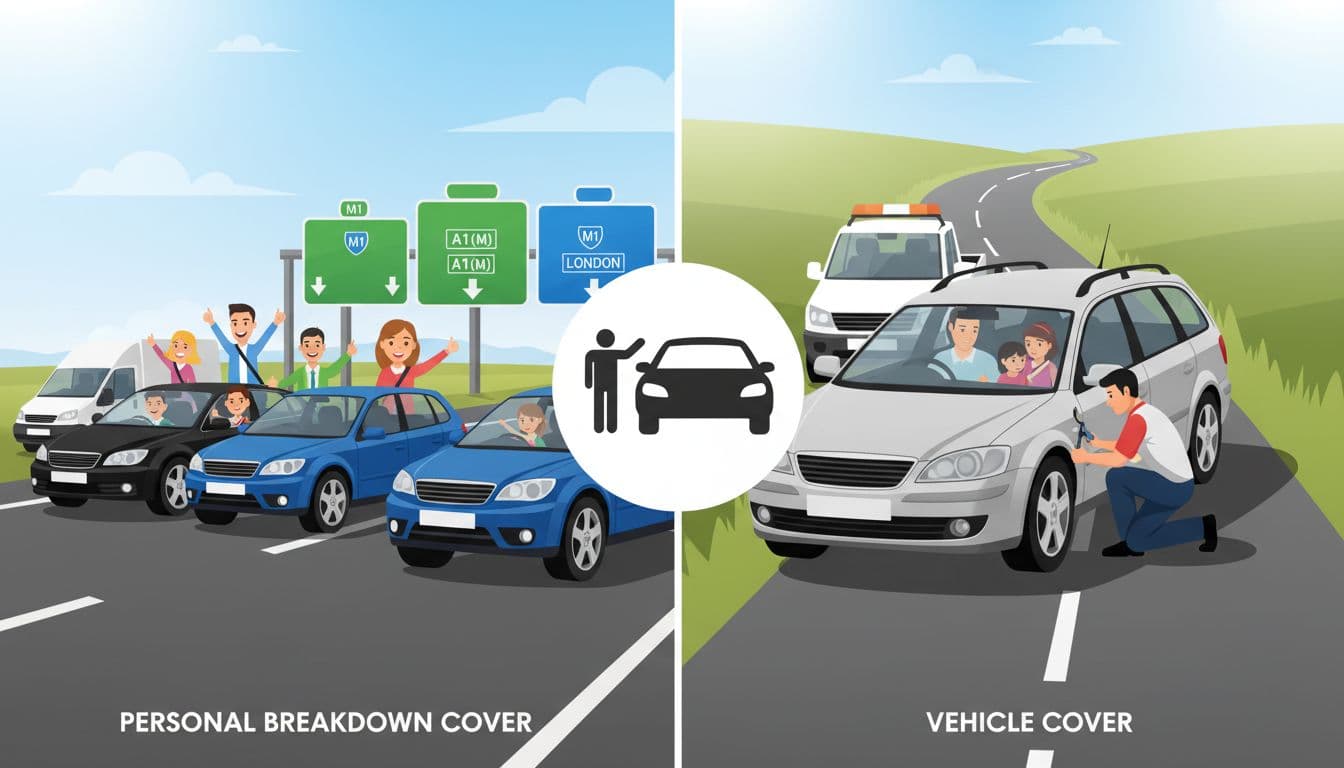

Personal vs vehicle breakdown cover, what is the difference in plain English?

Personal cover follows the person, vehicle cover follows the car, created with AI.

Personal cover follows the person, vehicle cover follows the car, created with AI.

The easiest way to remember it is this:

- Personal breakdown cover follows you. If you’re driving (or sometimes travelling as a passenger), you can get help in many vehicles, even if you don’t own them.

- Vehicle breakdown cover follows one specific vehicle. If that car breaks down, help can be sent, no matter who is driving.

A few quick examples make it click:

- You drive your own car: either type can work.

- You drive your partner’s car: personal cover often still covers you, vehicle cover only helps if that car is the one insured.

- You borrow a friend’s car: personal cover may help, vehicle cover usually won’t unless your friend has covered that car.

- You’re a passenger on a trip: some personal policies include passenger cover, some don’t, so you’d need to check.

In the UK, breakdown products often bundle service levels. The names vary, but you’ll commonly see: at-home assist, roadside assistance, recovery, and onward travel. The type of policy (personal or vehicle) decides who or what is insured, while the service level decides how far the help goes.

A simple comparison:

FeaturePersonal breakdown coverVehicle breakdown coverWhat’s insured?You (as a person)A specific carWho can use it?Usually the named person (sometimes a partner add-on)Usually any driver of that carBest forPeople who use different carsHouseholds sharing one main carWeak spotOther drivers may need their own coverDoesn’t help in other cars

Personal breakdown cover: when it saves you money (and when it does not)

Personal cover often gives better value when your life involves more than one set of car keys. It’s like having a coat that fits you, not a coat that fits one chair in your house.

Personal cover can be a strong fit if:

You drive different cars. Maybe you share cars in the family, you use a courtesy car, or you drive a relative’s vehicle now and then. A vehicle-only policy can’t follow you into those situations.

Your household has more than one car, but you’re the main driver of both. One personal policy can sometimes protect you across both, which can work out cheaper than covering each vehicle separately.

You often end up rescuing other people’s plans. If you’re the one who offers to drive, personal cover can protect you even when the car isn’t yours (as long as your policy allows it).

Where personal cover can lose value:

If you rarely travel in other vehicles, you’re paying for flexibility you don’t use. If you share driving equally, your partner may also need their own personal policy, which can double the cost.

It can also fall short if the policy excludes the vehicle type you use most, such as some vans, certain business use, or vehicles outside specific weight and size limits. Always check what counts as an “eligible vehicle”.

Vehicle breakdown cover: when it is better value (and when it does not)

Vehicle cover is often the simplest option. It’s tied to the car, and anyone driving that car can usually call for help. For many UK households, that’s exactly what they need.

Vehicle cover tends to be better value if:

You have one main car and it’s the car that does most journeys. If that car fails, you want a straightforward rescue plan.

Several drivers use the same car. A couple, a family with a new driver, or a shared “house car” often suits vehicle cover because the protection is about the car, not one named person.

You want fewer “who’s covered?” surprises. With vehicle cover, the question often becomes “is this the covered car?”, which is easy to answer.

Where vehicle cover can lose value:

If you break down in another car, you’re often on your own. If you change cars mid-term, you may need to update the policy or re-buy cover, depending on the provider’s rules.

It can also get expensive if you cover several vehicles separately when one personal policy would have covered the main driver in all of them.

What “better value” really means for breakdown cover (beyond the price)

The cheapest policy can still be poor value if it doesn’t work when you need it most. Value is the balance of price plus usefulness in your real life.

When comparing personal vs vehicle breakdown cover, focus on outcomes:

- Who is covered: just you, you and a partner, any driver, passengers?

- Where you’re covered: at home, on the road, on private land, at work car parks?

- What happens if the car can’t be fixed: do you get towed, and how far?

- What happens next: do you get a hire car, a hotel, or travel costs paid?

- Limits and exclusions: how many call-outs, what’s not included, and what counts as “fair use”.

Think of breakdown cover like an umbrella. A cheap one still counts, but not if it turns inside out in the first gust.

Compare the benefits that change the real cost: at-home assist, recovery, onward travel

Recovery and onward travel benefits matter when a quick roadside fix isn’t possible, created with AI.

Recovery and onward travel benefits matter when a quick roadside fix isn’t possible, created with AI.

These add-ons are where the “real cost” changes, because they decide whether you’re merely safe at the roadside, or actually able to finish your day.

At-home assist helps when the car won’t start at your home address (or sometimes near it). This is a common UK call-out, especially with flat batteries.

Recovery is the tow or transport when the car can’t be fixed quickly. Some policies take you to a nearby garage, some take you to a destination you choose, within limits.

Onward travel is the backup plan after recovery. Depending on the policy, that could mean a hire car, a hotel, or public transport costs. It often has caps, time limits, and conditions (for example, only if the breakdown is a set distance from home).

A cheap roadside-only policy can look fine until you’re stuck 60 miles from home on a Sunday evening. Matching benefits to your most likely breakdown scenario is where value shows up.

Hidden limits to check before you buy: call-outs, mileage, vehicle age, and exclusions

Most disappointment comes from limits people didn’t spot. A quick scan of the summary of cover and exclusions can save you a lot of grief.

Here are the practical checks that often affect whether you can claim:

Call-outs and “fair use”: some policies quote unlimited call-outs but still apply a fair use rule. Others cap the number. If you drive an older car, this matters.

Recovery limits: check if recovery is included at all, and if it has a mileage cap. A “local tow” can be very different from being taken home.

Waiting periods: some cover doesn’t start straight away, especially if you buy after a problem appears.

Common exclusions: look for wording on tyres, batteries, misfuelling, locked-in keys, and repeat faults. Some policies help, some treat these as non-covered incidents.

Maintenance-related failures: breakdown cover isn’t a substitute for servicing. If the issue is judged to be down to neglect, you may be refused help beyond basic safety support.

Vehicle rules: older, modified, imported, or heavier vehicles can have extra conditions. If you drive a van for work, check business use, size, and weight limits.

Which option is best for you? Quick UK scenarios and a simple decision guide

This section is the one to bookmark. Start with your real pattern, not your ideal one.

A simple decision guide:

- If you share one main car with other drivers, vehicle cover often gives better value.

- If you drive more than one car, personal cover often gives better value.

- If you borrow cars, drive courtesy cars, or travel as a passenger often, personal cover is usually safer.

- If you rarely drive, don’t overpay, but do check whether your most likely problem is at-home non-starts.

- If you do long trips for work or family, prioritise recovery and onward travel, whatever cover type you choose.

Best for households: one car, two drivers, or several cars

Household set-ups change which type of cover offers better value, created with AI.

Household set-ups change which type of cover offers better value, created with AI.

One shared car, two drivers: vehicle cover often wins because both drivers can call for help, and you’re paying to protect the car that does the miles.

Two cars, one person drives both: personal cover can win because one policy may follow the main driver across both vehicles.

Families with multiple drivers and multiple cars: it’s rarely one-size-fits-all. If different people regularly drive different cars, you might mix cover types, or accept that each regular driver needs personal cover if you want “cover follows the driver” flexibility.

The key point: value depends on who drives what, not just how many cars you own.

Best for lifestyle: commuters, city drivers, occasional drivers, and older cars

Commuters often get the most value from recovery and onward travel. Missing a shift or an appointment can cost more than the policy, especially if you rely on one route and one car.

City drivers may prioritise fast roadside attendance and at-home assist. Short trips, stop-start traffic, and battery drain can trigger non-starts more than people expect.

Occasional drivers can keep costs down with basic cover, but it’s still worth having recovery if your “one big trip” is a long motorway run to see family.

Older cars are not a reason to panic-buy every add-on. They are a reason to be honest. If you’ve had repeated faults or you’re running on thin tyres and a tired battery, broader cover can pay off, but it won’t fix underlying maintenance.

Choose cover based on risk you can explain in one sentence, like “I do long trips twice a month” or “my car often won’t start in winter”.

How to buy breakdown cover smarter in the UK (and avoid paying twice)

Comparing cover at home helps you avoid duplicate add-ons and missed limits, created with AI.

Comparing cover at home helps you avoid duplicate add-ons and missed limits, created with AI.

The smart way to buy breakdown cover is boring, but it works: list what you already have, list what you actually need, then pay only for the gap.

People often pay twice without realising, or they buy a cheap level of cover that doesn’t match their most likely breakdown.

Check for existing cover first: car warranty add-ons, bank accounts, and manufacturer assistance

You might already have some roadside help through a packaged bank account, a car warranty add-on, a new-to-you car package, or manufacturer assistance. Car insurance can also include optional breakdown cover.

Before you buy anything else, confirm: the level of cover (roadside only or recovery too), whether at-home assist is included, who is covered (you, any driver, named drivers), and any vehicle limits.

It’s not unusual to find you’re already covered for the basics, but missing recovery or onward travel.

Questions to ask before you commit: who is covered, where you are covered, and what happens next

Use this as a quick buyer checklist:

- Does it cover breakdowns at home, or only on the road?

- Does it cover any driver, or only the named person?

- If it’s personal cover, am I covered when driving other cars?

- Is recovery included, and how far can I be towed?

- What does onward travel pay for, and what are the limits?

- Are there waiting periods before cover starts?

- What counts as an excluded breakdown (battery, tyres, repeat faults, keys, misfuelling)?

- Is there a fair use rule, even if call-outs are “unlimited”?

- What is the cancellation policy, and can I change the vehicle details easily?

Conclusion

Better value comes from matching the cover to how you actually travel. Personal breakdown cover usually offers stronger value if you drive different vehicles, borrow cars, or often help family and friends. Vehicle breakdown covercan be better value when one main car is shared by several drivers.

Before you commit, compare like-for-like benefits such as at-home assist, recovery, and onward travel, because that’s where cheap policies can fall short. Write down your most common journeys and who drives, then choose the cover type that fits your real week, not the one you wish you had.

Shop Breakdown Cover

Shop for More with Our Verified UK Insurance providers:

Home Emergency Cover Home Appliance Cover– Income Protection insurance

Travel Insurance – Gadget Insurance – Phone Insurance – Caravan Insurance – Cycle Insurance – E-Bike Insurance

Car Finance – Car Breakdown Cover – Van Breakdown Cover – Motorbike Breakdown Cover

–

Explore our Buyers Guides with Money Saving Tips

For a list of our main buyers guides use the drop-down menu at the top of the page. Topics related to this article are:

Laptop Insurance Buyers Guides

Gadget Insurance Buyers Guides

Tennant’s Insurance Buyers Guide

Landlords Insurance Buyers Guide

Home Emergency Cover Buyers Guide

Travel Insurance Buyers Guides

Car Breakdown Cover Buyers Guide

–

Comments

Post a Comment